Statistical & Financial Consulting by Stanford PhD

Home Page

KENDALL'S TAU

= \textrm{P}\bigl((X_1 - X_2)(Y_1 - Y_2) > 0\bigr) - \textrm{P}\bigl((X_1 - X_2)(Y_1 - Y_2) < 0\bigr).\ \ \ \ \ \ \ \textbf{(1)})

If and

and

have continuous marginal distributions then

have continuous marginal distributions then

) has the same units as Pearson's correlation. Just like Pearson's correlation it covers the whole range of [-1,1], but now -1 corresponds to a perfect negative relationship (

has the same units as Pearson's correlation. Just like Pearson's correlation it covers the whole range of [-1,1], but now -1 corresponds to a perfect negative relationship ( is any decreasing deterministic function of ) and 1 corresponds to a perfect positive relationship ( is any increasing deterministic function of ). When

or

has a discrete mass, interval [-1,1] is not covered fully. For example, if variable

takes a given value with positive probability p, then with probability of at least p2 there is a tie:

is any decreasing deterministic function of ) and 1 corresponds to a perfect positive relationship ( is any increasing deterministic function of ). When

or

has a discrete mass, interval [-1,1] is not covered fully. For example, if variable

takes a given value with positive probability p, then with probability of at least p2 there is a tie:

And so

falls into interval [-1 + p2, 1 - p2]

no matter what the bivariate relationship is. There are several proposals on how to adjust for ties, the most obvious one being to divide formula (1) by

And so

falls into interval [-1 + p2, 1 - p2]

no matter what the bivariate relationship is. There are several proposals on how to adjust for ties, the most obvious one being to divide formula (1) by

(Y_1 - Y_2) = 0\bigr).)

Still, no single generalization has been widely accepted.

Note that definition (1) depends on ranks only. We only care if is bigger than

is bigger than

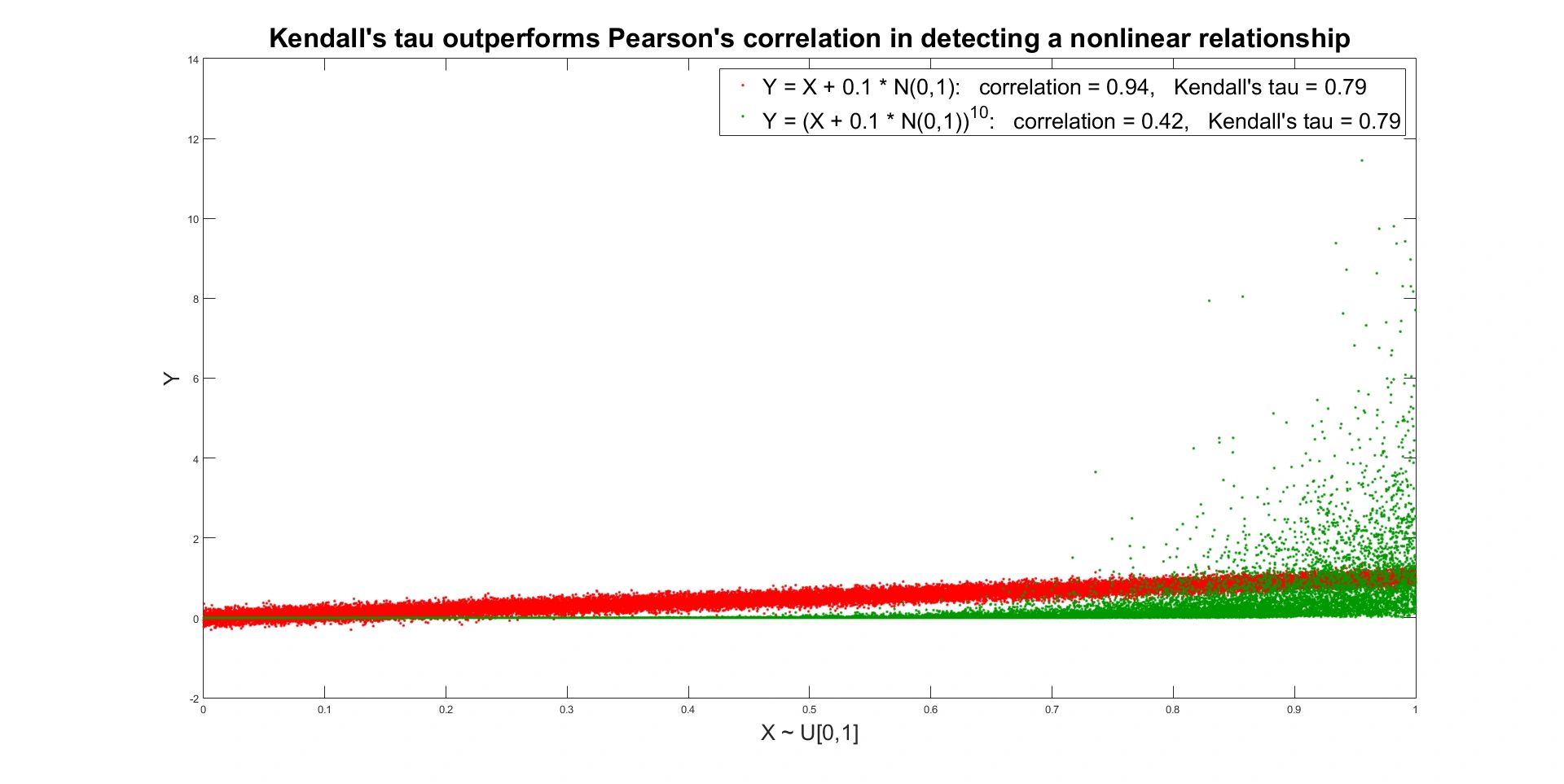

the actual values being irrelevant. So Kendall's tau is invariant to any monotonically increasing nonlinear transformations of

and

the actual values being irrelevant. So Kendall's tau is invariant to any monotonically increasing nonlinear transformations of

and  If we raise

to the third power Kendall's tau will stay the same. This is very important. Kendall's tau is naturally built to capture the strength of highly nonlinear relationships, where traditional linear association measures fail. The following graph illustrates the fact.

If we raise

to the third power Kendall's tau will stay the same. This is very important. Kendall's tau is naturally built to capture the strength of highly nonlinear relationships, where traditional linear association measures fail. The following graph illustrates the fact.

Kendall's tau has direct relation to the copula function) generated by random variables

and

generated by random variables

and

= 4 \int\int_{[0,1]^2} C(u,v)\ dC(u,v) - 1.)

The copula function does not depend on marginal distributions and captures what happens to

and

if they are transformed into random variables uniformly distributed on [0,1]. The formula above signals once again that Kendall's tau does not depend on marginal distributions of

and

and is invariant to any monotonically increasing transformations of

and

Several sample estimators have been developed. Let, ..., (X_n,Y_n)) denote observations from the joint distribution of

and

Pairs

denote observations from the joint distribution of

and

Pairs

) and

and

) are called

are called

concordant if their ranks agree: or

or

discordant if their ranks disagree: or

or

tied if or

or

Let

number of concordant pairs,

number of concordant pairs,

number of discordant pairs,

number of discordant pairs,

number of unique values in

number of unique values in

number of unique values in

number of unique values in

number of tied values in the i-th group of ties in

number of tied values in the i-th group of ties in

number of tied values in the j-th group of ties in

number of tied values in the j-th group of ties in

}{2},)

}{2},)

}{2}.)

The estimators of

are defined as

(N-N_Y)}},)

}{(q-1)n^2}.)

Estimators and

and

make adjustments for ties and are suitable for all distributions.

Estimator

make adjustments for ties and are suitable for all distributions.

Estimator

does not adjust for ties and is suitable only for continuous distributions measured with high precision.

Each of the estimators

does not adjust for ties and is suitable only for continuous distributions measured with high precision.

Each of the estimators

is nonparametric in the sense that it makes little or no assumptions about the joint distribution of

and

In particular, no functional form is postulated for the conditional expectation of

given

and the conditional expectation of

given

For each of the estimators

tests have been developed, telling us if

equals 0. A typical test is based on a transformation of the estimator which is asymptotically normal (its distribution converges to a normal distribution when the sample size grows big).

is nonparametric in the sense that it makes little or no assumptions about the joint distribution of

and

In particular, no functional form is postulated for the conditional expectation of

given

and the conditional expectation of

given

For each of the estimators

tests have been developed, telling us if

equals 0. A typical test is based on a transformation of the estimator which is asymptotically normal (its distribution converges to a normal distribution when the sample size grows big).

KENDALL'S TAU REFERENCES

Nelsen, R. B. (2006). An Introduction to Copulas (2nd ed). New York: Springer.

Salvadori, G., De Michele, C., Kottegoda, N. T., & Rosso, R. (2007). Extremes in Nature: An Approach Using Copulas. Springer.

Gibbons, J. D., & Chakraborti, S. (2003). Nonparametric Statistical Inference (4th ed). New York: Marcel Dekker.

Nešlehová, J. (2007). On Rank Correlation Measures for Non-continuous Random Variables. Journal of Multivariate Analysis, Vol. 98, Issue 3, pp. 544-567.

Kendall, M. (1938). A New Measure of Rank Correlation. Biometrika, Vol. 30 (1–2), pp. 81–89.

BACK TO THE STATISTICAL ANALYSES DIRECTORY

IMPORTANT LINKS ON THIS SITE

Kendall's Tau (Kendall's Rank Correlation Coefficient) is a measure of nonlinear dependence between two random variables. If random variables

and

have joint distribution

and random vectors

and

are independent realizations from that distribution, then Kendall's tau of

and

equals

If

Still, no single generalization has been widely accepted.

Note that definition (1) depends on ranks only. We only care if

Kendall's tau has direct relation to the copula function

The copula function does not depend on marginal distributions and captures what happens to

Several sample estimators have been developed. Let

concordant if their ranks agree:

discordant if their ranks disagree:

tied if

Let

The estimators of

Estimators

KENDALL'S TAU REFERENCES

Nelsen, R. B. (2006). An Introduction to Copulas (2nd ed). New York: Springer.

Salvadori, G., De Michele, C., Kottegoda, N. T., & Rosso, R. (2007). Extremes in Nature: An Approach Using Copulas. Springer.

Gibbons, J. D., & Chakraborti, S. (2003). Nonparametric Statistical Inference (4th ed). New York: Marcel Dekker.

Nešlehová, J. (2007). On Rank Correlation Measures for Non-continuous Random Variables. Journal of Multivariate Analysis, Vol. 98, Issue 3, pp. 544-567.

Kendall, M. (1938). A New Measure of Rank Correlation. Biometrika, Vol. 30 (1–2), pp. 81–89.

BACK TO THE STATISTICAL ANALYSES DIRECTORY

IMPORTANT LINKS ON THIS SITE

- Detailed description of the services offered in the areas of statistical and financial consulting: home page, types of service, experience, case studies, payment options and actuarial science tutoring

- Directory of financial topics